The Tax Foundation respectfully submits comment on the state tax and revenue implications of the proposed tobacco product standard for menthol in cigarettes. Alongside the intended consequence of limiting sales of menthol cigarettes, menthol cigarette prohibition will have a significant impact on state revenue collections, in excess of the losses associated with individuals who respond in keeping with desired policy outcomes (e.g., giving up or never beginning smoking). Given the high level of taxation on tobacco products—on average, excise taxes alone make up 40 percent of the retail price—a menthol prohibition will assuredly reduce revenues both for federal and state governments, while it is less likely that the policy will yield significant benefits in terms of smoking cessation.

If the Food and Drug Administration bans menthol cigarettes, federal and state governments, combined, stand to lose more than $6.6 billion in the first full year following prohibition.

Prohibiting flavors in combustible tobacco products is not without precedent. Multiple international jurisdictions have already banned the sale of non-tobacco flavored cigarettes—among them the European Union and Canada. In the U.S., several localities have banned the sale as well, as have Massachusetts and the District of Columbia. The major difference between the U.S. and most other tobacco markets is the non-tobacco flavored cigarette market share. Both in Canada and Europe, non-tobacco flavors made up less than 10 percent of the market, so the bans impacted a relatively minor consumer group. In the U.S., menthol flavored cigarettes make up more than one-third of the total market, and are particularly popular with African-American smokers, 75 percent of which consume non-tobacco flavored products.

It stands to reason that if consumption truly disappeared as a result of prohibition, and taxes on tobacco and nicotine products were genuinely intended to account for the harms caused by the products, no one would be worried about such a loss in revenue—if consumption is gone, so are the societal costs associated with consumption. This analysis shows, however, that consumption does not disappear, and that revenue from taxes on tobacco products is rarely used to offset harm caused by that consumption.

The Massachusetts ban, which is the primary U.S. experience to date, has not achieved its goals. After one year, sales in the state had dropped by 24 percent, but 90 percent of that decline in sales merely represented purchases shifting to neighboring states. The result of the policy has been a fairly stable level of consumption but a $125 million decline in excise tax revenue. In other words, Massachusetts is stuck with the costs associated with tobacco consumption but without the revenue from taxing tobacco products. [1] According to the state’s own Multi-Agency Illicit Tobacco Task Force, there was an increase in the smuggling of flavored cigarettes (as well as other flavored tobacco and nicotine products): “The increase in seizures of flavored ENDS products and menthol cigarettes combined with the decrease in revenue for cigarettes and OTP likely indicates increased cross-border smuggling of these products.”[2]

Of course, Massachusetts consumers can easily purchase menthol cigarettes in other states, whereas a nationwide ban increases the costs of acquiring the products. But by extrapolating the trends observed in the European Union (the only other region-wide ban), we can offer an estimate of how consumers may react if a nationwide ban is imposed. In Europe, approximately 90 percent of cigarette consumers continued to consume but either engaged in cross-border trade, switched to other flavored tobacco products, or started smoking non-flavored cigarettes. Among the relatively small group of menthol smokers, about 8 percent of consumers reported quitting after the ban.[3]

Under these assumptions, more than half of the market would remain taxed, but slightly more than 40 percent of consumption would move into other legal tobacco or nicotine use (some taxed at lower rates and some not taxed at all) or illicit tobacco use. In our assumptions, around 20 percent of current menthol cigarette consumption will move to completely untaxed consumption. A very similar experience was observed in Canada—despite continued limited access to menthol products on the legal market. In Canada, 60 percent of menthol smokers switched to non-menthol, 21 percent either quit tobacco or switched to non-combustibles, and 20 percent continued to consume menthol.[4]

The following estimates include only cigarettes, which represent more than 90 percent of revenue from tobacco taxes. Cigarettes face a $1.01 a pack federal tax and an average of $1.91 in state taxes. Additionally, cigarettes are generally included in sales tax bases. Moreover, every state party to the agreement receives a share of the Master Settlement Agreement (MSA),[5] which translates to about $0.75 per pack in 2022.

It is worth noting that the estimates of cross-border trade in Europe (13 percent of menthol smokers) are self-reported (and thus likely underreported due to illegality), and real illicit trade could be significantly higher in the U.S. since the size of the menthol market makes it a much more profitable market for illicit trade.

While cross-border trade would become more difficult with a nationwide ban, there is nothing to suggest that it would greatly hamper the growth of illicit sales, as has been experienced with cannabis. Illicit trade[6] is already a major issue in many states and offering competitive advantages to smugglers would only make the issue bigger—especially since all indications are that the FDA will not enforce against possession or consumption.[7]

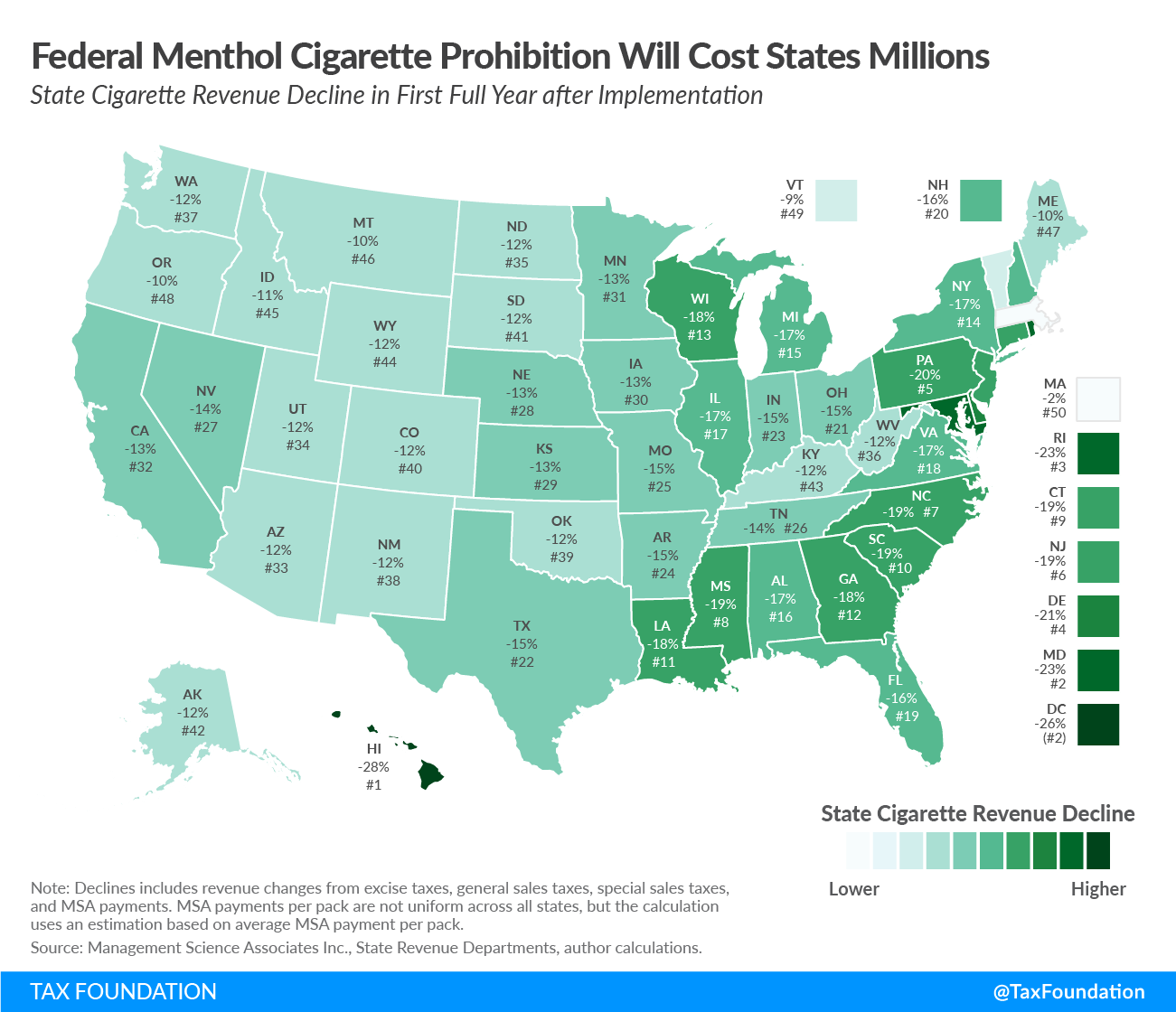

A nationwide ban would result in a federal revenue decline of $1.9 billion in the first full year after prohibition. In the states, the decline in excise tax revenue would be $2.6 billion, in sales tax revenue would be $892 million, and in MSA payments would be $1.2 billion, for a total state revenue loss of $4.7 billion. A relatively small portion of the revenue loss would be offset by increases in taxes from other tobacco products, which could still be sold flavored. Both state governments and the federal government would experience significant decreases to their tobacco tax revenue without experiencing a corresponding decrease in consumption.

| State | Menthol cigarettes share of market | Excise tax rate per pack of 20 cigarettes | Total revenue decline | Excise tax decline as percentage of total decline |

|---|---|---|---|---|

| Alabama | 42% | $0.675 | -$83,087,724 | 36% |

| Alaska | 24% | $2.00 | -$7,403,636 | 62% |

| Arizona | 26% | $2.00 | -$60,425,192 | 53% |

| Arkansas | 33% | $1.15 | -$52,609,248 | 44% |

| California | 27% | $2.87 | -$328,526,977 | 63% |

| Colorado | 24% | $1.94 | -$46,266,930 | 39% |

| Connecticut | 43% | $4.35 | -$80,529,512 | 78% |

| Delaware | 51% | $2.10 | -$30,932,062 | 81% |

| District of Columbia | 64% | $4.50 | -$6,056,103 | 86% |

| Florida (a) | 38% | $1.339 | -$307,925,101 | 53% |

| Georgia | 47% | $0.37 | -$123,466,776 | 28% |

| Hawaii | 68% | $3.20 | -$37,642,114 | 80% |

| Idaho | 18% | $0.57 | -$11,511,087 | 24% |

| Illinois | 39% | $2.98 | -$221,663,232 | 67% |

| Indiana | 33% | $0.995 | -$119,399,578 | 44% |

| Iowa | 27% | $1.36 | -$43,399,368 | 49% |

| Kansas | 28% | $1.29 | -$31,002,040 | 47% |

| Kentucky | 23% | $1.10 | -$85,408,770 | 43% |

| Louisiana | 44% | $1.08 | -$99,943,842 | 47% |

| Maine | 18% | $2.00 | -$17,845,224 | 51% |

| Maryland | 57% | $3.75 | -$125,430,426 | 69% |

| Massachusetts | 0% | $3.51 | -$11,709,397 | -1% |

| Michigan | 41% | $2.00 | -$218,768,220 | 65% |

| Minnesota (a) | 27% | $3.04 | -$91,549,892 | 70% |

| Mississippi (a) | 49% | $0.68 | -$55,206,327 | 41% |

| Missouri | 32% | $0.17 | -$88,549,975 | 12% |

| Montana | 17% | $1.70 | -$8,627,522 | 52% |

| Nebraska | 28% | $0.64 | -$18,864,991 | 32% |

| Nevada | 32% | $1.80 | -$41,266,683 | 56% |

| New Hampshire | 34% | $1.78 | -$49,376,205 | 71% |

| New Jersey | 45% | $2.70 | -$154,696,289 | 71% |

| New Mexico | 24% | $2.00 | -$16,458,142 | 54% |

| New York | 40% | $4.35 | -$224,654,441 | 73% |

| North Carolina | 48% | $0.45 | -$164,733,092 | 33% |

| North Dakota | 22% | $0.44 | -$8,511,164 | 22% |

| Ohio | 34% | $1.60 | -$227,107,134 | 56% |

| Oklahoma | 24% | $2.03 | -$60,218,857 | 66% |

| Oregon | 18% | $3.33 | -$35,816,949 | 61% |

| Pennsylvania | 48% | $2.60 | -$352,089,325 | 71% |

| Rhode Island | 53% | $4.25 | -$44,896,541 | 78% |

| South Carolina | 48% | $0.57 | -$81,979,933 | 37% |

| South Dakota | 24% | $1.53 | -$10,270,759 | 50% |

| Tennessee | 32% | $0.62 | -$102,194,090 | 30% |

| Texas (a) | 34% | $1.41 | -$327,792,926 | 53% |

| Utah | 25% | $1.70 | -$17,543,134 | 51% |

| Vermont | 18% | $3.08 | -$8,133,443 | 61% |

| Virginia | 45% | $0.60 | -$121,654,633 | 39% |

| Washington | 25% | $3.025 | -$58,476,364 | 62% |

| West Virginia | 24% | $1.20 | -$36,930,563 | 44% |

| Wisconsin | 41% | $2.52 | -$133,748,424 | 70% |

| Wyoming | 19% | $0.60 | -$5,196,027 | 26% |

| Federal | 36% | $1.01 | -$1,877,312,548 | 100% |

| Total | -$6,574,808,933 | 68% | ||

|

Note: Declines includes revenue changes from excise taxes, general sales taxes, special sales taxes, and MSA payments. MSA payments per pack are not uniform across all states, but the calculation uses an estimation based on average MSA payment per pack. (a) These states have separate settlement agreements with the tobacco industry and are not party to the MSA. Sources: Management Science Associates Inc., state revenue departments, author calculations. |

||||

The size of the non-tobacco flavored market differs by state (figures in Table 1), and the estimates reflect these differences. At a national level, menthol flavored cigarettes make up roughly 36 percent of the market.

Revenue from excise taxes and MSA payments are commonly earmarked for designated spending priorities. The federal government spends excise tax revenue on health-care costs, and the states spend their revenue on a wide variety of priorities—although rarely enough on cessation programs.[9] MSA payments are a more delicate matter. These payments are based on a calculation of inflationary developments and volume of sales in relation to a base volume and base payment set out in the settlement.[10] When the settlement was reached in 1998, projections for future payments were made based on estimates of market developments, but they have turned out to be overly optimistic. In 2018, the projection was off by $2.7 billion, or roughly 27 percent.[11]

Despite these failed projections, many states rely on this revenue since the payments are supposed to continue in perpetuity (or as long as cigarettes are sold by participating manufacturers). One popular policy has even been to securitize the payments to secure large up-front payments and use the annual payments to pay bond holders. While this arrangement is mostly a risk to the investors, there has been speculation that states could be pressured to meet their payment obligations using general fund revenue in the event of significant MSA payment reductions.[12] Despite not being obliged, New Jersey bailed out tobacco bonds headed for default in 2014, and in Pennsylvania, Act 43 of 2017 permits general tax revenue to be used for debt service on the state’s tobacco bonds.[13]

The following table includes appropriations from 12 states, but these practices are common across all 50 states and the District of Columbia. The table has a topline description of how revenue is spent in many states, and it illustrates what kind of programs will see reduced funding if prohibition is imposed. The appropriations are numerous and can be very specific. In Arizona, for instance, the tobacco products tax fund distributes revenue as follows (per $1):

- Health education account: 2 cents

- Medically needy account: 27 cents

- Emergency health services account: 20 cents

- Health care adjustment account: 4 cents

- Health care cost containment account (AHCCCS): 42 cents

- Health research account: 5 cents[14]

The state has several other funds that receive revenue from taxes on tobacco products.

| State | MSA revenue CY 2021 | MSA Appropriations | Cigarette Excise Tax Revenue FY 2021 | Excise Tax Appropriations |

|---|---|---|---|---|

| Arizona | $106 million | Health Care Cost Containment System (AHCCCS) for persons who are uninsured | $269 million | Early childhood development programs for children prior to kindergarten and their families; health care; correctional facilities; substance abuse treatment; general fund |

| Florida (a) | $403 million | Tobacco cessation; Agency for Health Care Administration | $970 million | Biomedical research; teacher training; the Division of Alcoholic Beverages and Tobacco; general fund |

| Georgia | $176 million | Low-income Medicaid; Community Care Services; cancer treatment and prevention | $162 million | General fund |

| Illinois (b) | $283 million | Tobacco bond payments | $840 million | General fund; the Capital Projects Fund (clean water projects, wildlife conservation, infrastructure etc.); Healthcare Provider Relief Fund; the School Infrastructure Fund; the Long-Term Care Provider Fund |

| Kentucky | $126 million | Soil and water conservation; substance abuse treatment; public health; debt service; early childhood education | $356 million | Public health; Governor’s Office of Agricultural Policy; early childhood education; cancer research and screening; general fund |

| Michigan | $312 million | Tobacco bond payments; tourism marketing; business development; Detroit bankruptcy settlement; Detroit Public Schools Trust Fund; Medicaid | $776 million | Medicaid; school aid; health and safety; Healthy Michigan Fund (smoking cessation); general fund |

| Nevada | $44 million | Healthy Nevada Fund; family resource centers and disability services; Medicaid | $162 million | General fund; local governments |

| New Hampshire | $48 million | Education Trust Fund; general fund | $228 million | Education Trust Fund; general fund |

| New Jersey | $279 million | Tobacco bond payments | $546 million | General fund; health-care subsidies; debt service |

| New York (c) | $764 million | Medicaid; general fund; local governments | $920 million | General fund; health care |

| North Carolina | $167 million | Tobacco producers; general fund; community college system | $246 million | General fund; cancer research |

| Pennsylvania (d) | $362 million | Tobacco cessation; tobacco bonds; Medicaid; medical research; health-related purposes | $1,144 million | Refurbish the Tobacco Settlement Fund; general fund; Children’s Health Insurance Program; Agricultural Conservation Easement Purchase |

| Notes:

(a) Florida has a separate settlement agreement with the tobacco industry. It generally functions similarly to the Master Settlement Agreement. Details about payment schedule available here: http://edr.state.fl.us/content/conferences/tobaccosettlement/TobSettlementResults.pdf. (b) In 2010, Illinois sold substantially all payments under the MSA to fund outstanding obligations. Details in FY 2022 budget (page 510): https://www2.illinois.gov/sites/budget/Documents/Budget%20Book/FY2022-Budget-Book/Fiscal-Year-2022-Operating-Budget.pdf. (c) The state retired the last of its tobacco bond in fiscal year 2018. Until then, all payments were used for bond payments. (d) Following the state’s issuance of tobacco bonds, revenue from the tobacco tax has been transferred to the tobacco settlement fund to cover the annual debt service. Source: State statutes, state budgets, Tax Foundation research. |

||||

Tobacco excise taxes are already an unstable source of tax revenue.[15] Further narrowing the tobacco tax base by banning a portion of tobacco sales altogether could worsen the instability of this revenue source while driving up the costs of administration and law enforcement associated with prohibition, especially if the lost revenue is made up by raising the tax rate on the remaining tobacco tax base.

Government tax coffers are not all that is impacted by this ban, however. Bans impact the large number of small business owners operating tobacco shops, convenience stores, and gas stations. Policymakers and regulators should not lose sight of the law of unintended consequences as they set tax rates and regulatory regimes for nicotine products. The goal is to reduce smoking; the effect may simply be to shift consumers to other products, or to illegally acquired ones. The question of illegality may be especially problematic. While the FDA has said that a ban will not be enforced at the individual level, the vast majority of states have quite severe sentencing requirements for the possession of illicit tobacco products.

One of the reasons for prohibiting flavors is a desire to limit uptake of nicotine and tobacco products. It is not clear, however, that flavor bans will do much to accelerate an already impressive and under-publicized trend: only 1.5 percent of middle schoolers and high schoolers smoked in the last 30 days, and 7.6 percent of the same group vaped.[16] In 2019, the number of high schoolers who had vaped in the past 30 days was 27.5 percent, and 5.8 percent had smoked in the same period.[17]

If the national ban proves even a fraction as ineffective as the Massachusetts ban, it becomes a very expensive exercise in narrowing a tax base, which effectively leaves fewer taxpayers to cover the costs of the externalities associated with smoking. Moreover, the ban will further contribute to the tobacco tax’s lack of stability, resulting in some uncertainty for the government programs funded by these revenue streams.

[1] Ulrik Boesen, “Massachusetts Flavored Tobacco Ban: No Impact on New England Sales,” Tax Foundation, Feb. 3, 2022, https://www.taxfoundation.org/massachusetts-flavored-tobacco-ban-sales-jama-study/.

[2] Commonwealth of Massachusetts, “Annual Report of Multi-Agency Illegal Tobacco Task Force,” Mar. 1, 2022, https://www.mass.gov/doc/task-force-fy22-annual-report/download.

[3] Foundation for a Smoke-Free World, “EU Menthol Cigarette Ban Survey,” accessed Mar. 11, 2022, https://www.smokefreeworld.org/eu-menthol-cigarette-ban-survey-2/.

[4] Janet Chung-Hall, Geoffrey T Fong, Gang Meng, K Michael Cummings, Andrew Hyland, Richard J O’Connor, Anne C K Quah, and Lorraine V Craig, “Evaluating the impact of menthol cigarette bans on cessation and smoking behaviours in Canada: longitudinal findings from the Canadian arm of the 2016–2018 ITC Four Country Smoking and Vaping Surveys,” Tobacco Control (April 2021), https://tobaccocontrol.bmj.com/content/early/2021/03/31/tobaccocontrol-2020-056259.

[5] Forty-six states are part of the Master Settlement Agreement. The four remaining states have separate settlements.

[6] Ulrik Boesen, “Cigarette Taxes and Cigarette Smuggling by State, 2019,” Tax Foundation, Dec. 2, 2021, https://www.taxfoundation.org/state-tobacco-tax-cigarette-smuggling/.

[7] While the FDA is not going to enforce a ban on consumption of menthol cigarettes, states often have harsh penalties for engaging in illicit trade. See U.S. Food & Drug Administration, “FDA on Track to Take Actions to Address Tobacco-Related Health Disparities,” Jan 27, 2022, https://www.fda.gov/news-events/fda-voices/fda-track-take-actions-address-tobacco-related-health-disparities.

[8] Campaign for Tobacco-Free Kids, “U.S. Federal Issues Federal Tobacco Taxes,” Sept. 19, 2017, https://www.tobaccofreekids.org/what-we-do/us/federal-tobacco-taxes.

[9] Campaign for Tobacco-Free Kids, “U.S. State and Local Issues: Broken Promises to Our Children,” Jan 12, 2022, https://www.tobaccofreekids.org/what-we-do/us/statereport.

[10] National Association of Attorneys General, “MSA Payment Information,” accessed Mar. 25, 2022, https://www.naag.org/our-work/naag-center-for-tobacco-and-public-health/the-master-settlement-agreement/msa-payment-information/.

[11] Campaign for Tobacco-Free Kids, “Adjustments to The States’ Tobacco Settlement Receipts,” Jan. 10, 2001, https://www.tobaccofreekids.org/assets/factsheets/0070.pdf.

[12] Federal Reserve Bank of Boston, “New England Fiscal Facts,” Winter 2002/2003, 3, https://www.bostonfed.org/-/media/Documents/neff/tobacco.pdf.

[13] See Cezary Podkul, “Behind New Jersey’s Tobacco Bond Bailout, A Hedge Fund’s $100 Million Payday,” ProPublica, Dec. 30, 2014, https://www.propublica.org/article/behind-new-jerseys-tobacco-bond-bailout-a-hedge-funds-100-million-payday; Patrick Shaughnessy, “Budget Primer,” Pennsylvania House Appropriations Committee, Sept. 19, 2019, 4, https://houseappropriations.com/files/Documents/TobaccoSettlementFund_BP_Final_091919.pdf.

[14] State of Arizona, “Executive Budget Fiscal Year 2021,” January 2020, 420, https://azgovernor.gov/sites/default/files/fy_2021_s_u_of_state_funds_book_0.pdf.

[15] Ulrik Boesen and Tom VanAntwerp, “How Stable is Cigarette Tax Revenue?” Tax Foundation, May 3, 2021, https://www.taxfoundation.org/cigarette-tax-revenue-tool/.

[16] Centers for Disease Control and Prevention, “Tobacco Product Use and Associated Factors Among Middle and High School Students — National Youth Tobacco Survey, United States, 2021,” Mar. 11, 2022, https://www.cdc.gov/mmwr/volumes/71/ss/ss7105a1.htm?s_cid=ss7105a1_w.

[17] Karen A. Cullen, Andrea S. Gentzke, Michael D. Sawdey, et al., “E-Cigarette Use Among Youth in the United States, 2019,” JAMA 322:21 (December 2019): 2095-2103, https://www.ncbi.nlm.nih.gov/pmc/articles/PMC6865299/.