As part of his presidential campaign, President Biden embraced the “public option” and lowered the Medicare eligibility age. However, like most of this administration’s health policy agenda, these proposals have faded from public discussion over the past year and a half.but This week, the Congressional Budget Office (CBO) released analyze Lowering Medicare eligibility to age 60 has some interesting points and important caveats.

Revenue numbers for CBOs are relatively simple. Lowering the Medicare age to 60 would increase the federal deficit by $155 billion over six years (2026-2031), add 7.3 million to Medicare, reduce Employer-Sponsored Insurance (ESI) by 3.2 million, take action 1.8 million people moved from Medicaid to Medicare, reducing the uninsured population by approximately 400,000 by 2031 relative to the CBO’s baseline projection. So here are some observations.

First, all of this is an illusion. This is not a criticism – predictions are hard. However, the CBO’s current benchmark was released in July 2021 and, in hindsight, overly optimistic assumptions were made about how the economy would recover from the pandemic. The CBO will soon release an updated baseline that should better illustrate that the economic outlook is less optimistic than expected. This analysis would certainly be more useful if modeled on baseline assumptions that are closer to reality.

Second, deficit projections seem reasonable and consistent with analyze American Action Forum (AAF). The AAF projected last fall that reducing Medicare eligibility to 60 would increase the deficit by $380 billion over 10 years and about $211 billion over the same six-year period as CBO estimates.

third, Expanding Medicare does not significantly affect the number of Americans covered; instead, in the CBO’s analysis, it simply shuffles around those who already have coverage. This is a recurring theme in recent policy proposals aimed at expanding coverage.

Fourth, building on the previous point, despite much discussion of the roughly 28 million Americans who remain uninsured (though not always without insurance options), insurance-related policy proposals appear to be less and less designed to increase Insurance coverage, but to consolidate insurance coverage. Expanding Medicare, raising the income limit on the premium tax credit, and making it more generous, all to reduce the number of Americans enrolled in ESI and unsubsidized non-group coverage. Those aged 60-64 do not have to give up their ESI, but there is a risk of penalties in the future when they fail to register for Parts B and D when they are eligible. Additionally, the CBO expects many small employers to forgo coverage for those newly eligible for Medicare, removing the choice of whether to stay at ESI or switch to Medicare.

Policies that primarily move people from private health insurance to federal plans are effectively single-payer backdoor methods. It may not be a single federal program, but if everyone ends up being covered by a series of federal programs, that will produce roughly the same results. At the end of the day, adding $155 billion to the deficit to act as an insurance-covered musical chair doesn’t make much practical sense.

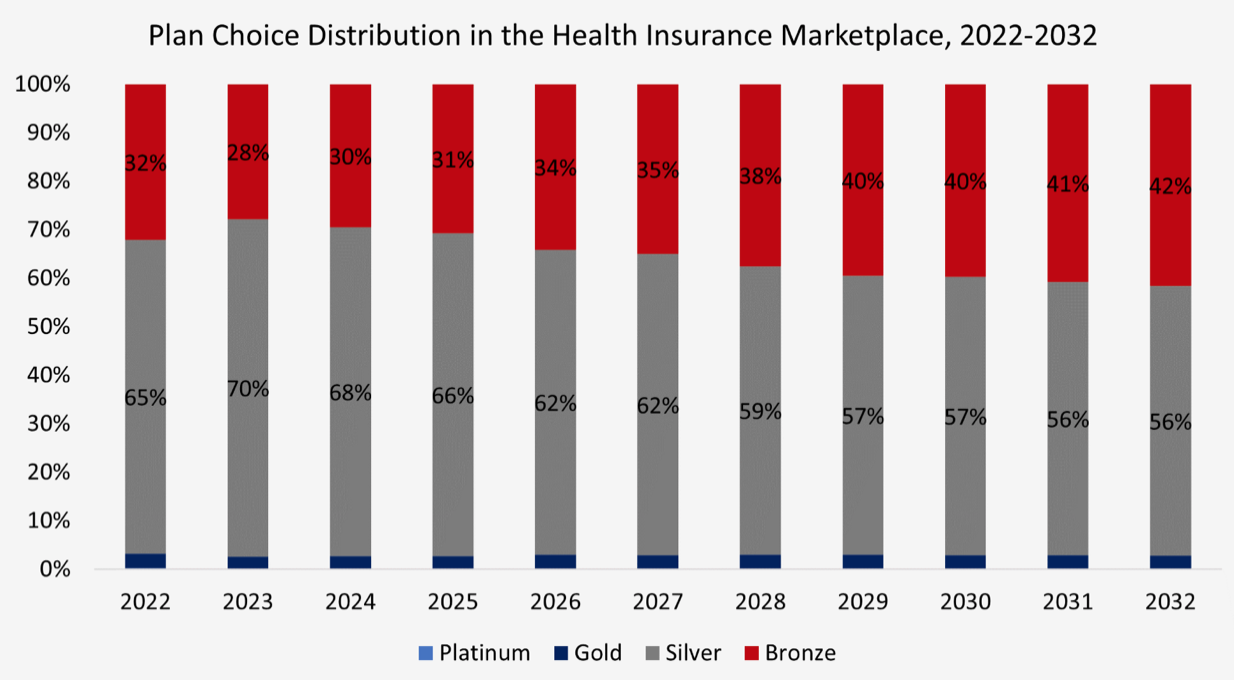

Chart Review: Distribution of Plan Choices in the Health Insurance Market 2022-2032

Margaret Barnhorsthealth care policy researcher

Earlier this week, the American Action Forum’s Center for Health and Economics (H&E) released its Annual Baseline Estimate, which includes 10-year projections of health insurance coverage, federal budget implications, plan choices, and premiums for Americans under 65 under current law. As premiums and healthcare costs rise over the next decade, and consumers with less subsidies adjust to higher premiums, H&E estimates that the plan of choice in the health insurance market will shift to lower-cost options. As shown in the chart below, Silver plans will continue to make up the majority of the market throughout the budget window, as cost-sharing benefits will only apply to silver plans in the market, although silver plan enrollments will be reduced as a percentage of all market plan choices. In 2022, 65% of Marketplace plan choices are Silver, 32% Bronze, about 3% Gold, and less than 0.2% Platinum. Plan choices for the higher-cost Gold and Platinum plans are largely unchanged over the next decade, but with time and premiums rising, the enrollment rate for Silver plans will drop to 56% of all market plan choices by 2032 %, while the enrollment rate for the Bronze program will rise to 42%.