in details and diagrams.

go through Wolf Richter for wolf street.

There is a lot of confusion about this “Real” GDP fell 1.4% month-on-month. So let me see what isn’t causing it, and what is causing it. The cause of it was a bizarre event that will likely begin to subside in the second quarter. We’ve seen some evidence.

What didn’t cause GDP to fall:

Consumer spending rose 2.7% The first quarter, the annual rate, was adjusted for sharp inflation. accounting for 70.5% of GDP. This increase was in the middle of the general range after the Great Recession until the pandemic (from 0.4% in the second quarter of 2011 to 4.5% in the fourth quarter of 2014).

However, there has been a clear shift from spending on goods to spending on services, especially discretionary services, which have collapsed during the pandemic.These discretionary services include airfare, sports and entertainment venues, cruise ships, more or less discretionary medical services (such as dentists, elective surgeries, routine doctor visits, etc. I discussed this Details of consumer spending shifting from goods to services. This shift in spending from goods to services will soon become important. This chart shows total consumer spending (in inflation-adjusted dollars) in GDP data:

Gross domestic private investment up 2.3% Annualized, following an astonishing surge in the fourth quarter. This measure includes investment in residential and non-residential structures, equipment, intellectual property, etc., and also includes “changes in private inventories” (more on this later).

Private inventories rose 5.7% In the first quarter, it was annualized and adjusted for strong inflation, following a 7.1% increase in the fourth quarter. Good sales in 2020 and 2021, particularly durable goods, have sparked a variety of supply chain issues and shortages, with U.S. companies running out of inventory in many commodity categories. They have been trying to catch up, and some supply chain issues improved late last year and earlier this year.

also, Consumer switching spending From goods where spending has been falling to services where spending has been soaring. Goods need to be stocked. Reduced demand for goods eased pressure on inventories. But inventories are still well below the levels needed for the economy to function smoothly:

Freak events that led to a drop in GDP in the first quarter:

Trade deficit in goods and services surges The first quarter fell by $192 billion on an annualized, inflation-adjusted basis, the second-largest drop ever in dollar terms, after the third quarter of 2020.

Exports are added to GDP and imports are subtracted from GDP. With exports rising modestly but imports soaring, “net exports” (exports minus imports) have had a negative impact on GDP for decades. During the pandemic, stimulus-fueled consumers have spent record amounts on goods, many of them imported, and the trade deficit has surged.

But the surge in the trade deficit that occurred last quarter was extraordinary. As supply chains improved, businesses were able to build inventories, and merchandise imports saw a historic increase, leading to a sharp deterioration in the merchandise trade deficit.

This brutal deterioration of the trade deficit reduces GDP by $192 billion a year. But overall GDP fell by only $70 billion! A halving in size (which will still be huge) will yield a positive GDP reading:

Why this bizarre trade deficit figure will start shrinking in the second quarter

In the next quarter or two, the trade deficit will be smaller than the anomalous performance in the first quarter, and a smaller drag on GDP. Why? because…

Consumer spending has shifted massively from goods (both adjusted for inflation) to services.

Spending on nondurable goods fell again in March on a seasonally and inflation-adjusted basis. It has been in decline since November and is down 0.8% from a year ago. But it’s still high, up 13% from 2019, and likely to slow further in the second quarter. Non-durable goods are mainly food, fuel and household goods.

Durable goods spending has fallen sharply since March 2021 (-10.7%, adjusted for inflation). But it remains high, up 24% from March 2019, and is likely to decline further, returning to pre-pandemic averages as consumers shift spending back to services:

Many of these goods are imported, and a reduction in spending on goods will lower import levels last year and in the first quarter of this year. This is not to say that the trade deficit will magically disappear, but it will go from scary to scary, and the trade deficit will become smaller and a much smaller drag on GDP.

Meanwhile, spending on services is surging. Even adjusted for inflation, it rose 0.6% in March and was up 6.3% year-on-year. But it’s still below pre-pandemic trends and has a long way to go to return to normal with above-normal growth, and we’ll see more of this normalization in the second quarter:

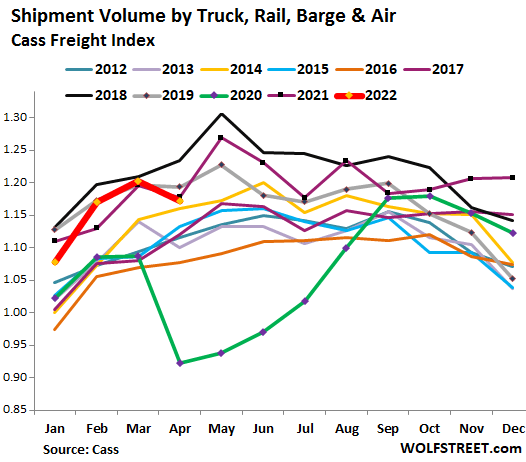

The sudden pullback in freight shipments indicated a slowdown in demand for goods in the second quarter.

We are already seeing a slowdown in U.S. shipments. This is comprehensive. According to the Cass Freight Index (my discussion: Freight Cycles, Freight and Signs of Decline in Demand). See bold red line:

Government consumption also fell in the first quarter.

Spending by federal, state, and local government agencies on equipment, supplies, fuel, and more (not wages and social spending) fell in the first quarter, which also weighed on GDP.

I’m not going to forecast government spending, but after the money printing spree and high taxes in 2021, governments at all levels are floating in a sea of cash. Sooner or later these governments will spend this money, which will boost GDP.

GDP decline in Q1 may ease in Q2.

Reducing catastrophic imports, and thus a catastrophic trade deficit, would reduce the drag on GDP. Consumers are holding out for now. After $11 trillion in stimulus over two years, there’s still plenty of money flowing among consumers, businesses and governments at the state and local levels, with $4.7 trillion coming from the Fed’s money printing presses, about 6 Trillions in government deficit spending. Some of that money will be spent over the next few quarters.

Yes, there will be a recession one day, because sooner or later there will always be, because recessions are part of the business cycle. But in the data so far, no recession has been outlined. Consumer spending on durable goods has retreated from its insane highs during the pandemic as spending shifts toward services, and overall spending growth is returning to pre-pandemic normal levels from a pandemic surge. This normalization is happening, and that’s a good thing.

When it comes to asset prices, however, a pull is taking place: After interest rate suppression and quantitative easing pushed almost all asset prices to often absurd levels, the Fed has already started raising rates and will soon begin quantitative tightening. So this is where the action will continue.

Enjoy reading WOLF STREET and want to support it? Use an ad blocker – I totally see why – but want to support the site? You can donate. I’m very grateful. Click on beer and iced tea mugs to learn how to:

Would you like to be notified by email when WOLF STREET publishes new articles? Register here.

![]()